AMD's 4Q/FY19 Financial Report: Revenue up 50% from 4Q18, Debt Halved

by Dr. Ian Cutress on January 28, 2020 4:51 PM EST- Posted in

- CPUs

- AMD

- GPUs

- Financial Results

AMD just announced its 4Q 2019 and Financial Year 2019 Earnings Report. Here are the key points, along with AMD's presentation.

Today AMD announced its 4Q 2019 revenue of $2.13 billion, up 18% from the previous quarter and up 50% from the same quarter last year. This is accompanied by a 45% gross margin for Q4, AMD's highest on record, up from 38% from Q4 last year and up from 43% in Q3. Operating income for the quarter was up a staggering 1143% (not a typo) from $28 million a year ago to $348 million this quarter, and net income was up 347% to $170 million. The resulted in earnings per share of $0.15, up 275% from a year ago.

| AMD Q4 2019 Financial Results (GAAP) | |||||

| Q4'2019 | Q3'2019 | Q4'2018 | Q/Q | Y/Y | |

| Revenue | $2127M | $1801M | $1419M | +18% | +50% |

| Gross Margin | 45% | 43% | 38% | +2% | +7% |

| Operating Income | $348M | $186M | $28M | +87% | +1143% |

| Net Income | $170M | $120M | $38M | +42% | +347% |

| Earnings Per Share | $0.15 | $0.11 | $0.04 | +36% | +275% |

For the full financial year, AMD is reporting revenue of $6.73 billion, up 4% from 2018, and a full year gross margin of 43%, up from 38%. Operating income was up 40% to $631 million, but net income was almost flat at $341 million. Earnings per share for the full year were down 6% to $0.30.

| AMD FY 2019 Financial Results (GAAP) | |||||

| FY'2019 | FY'2018 | Y/Y | |||

| Revenue | $6731M | $6475M | +4% | ||

| Gross Margin | 43% | 38% | +5% | ||

| Operating Income | $631M | $451M | +40% | ||

| Net Income | $341M | $337M | +1% | ||

| Earnings Per Share | $0.30 | $0.32 | -6% | ||

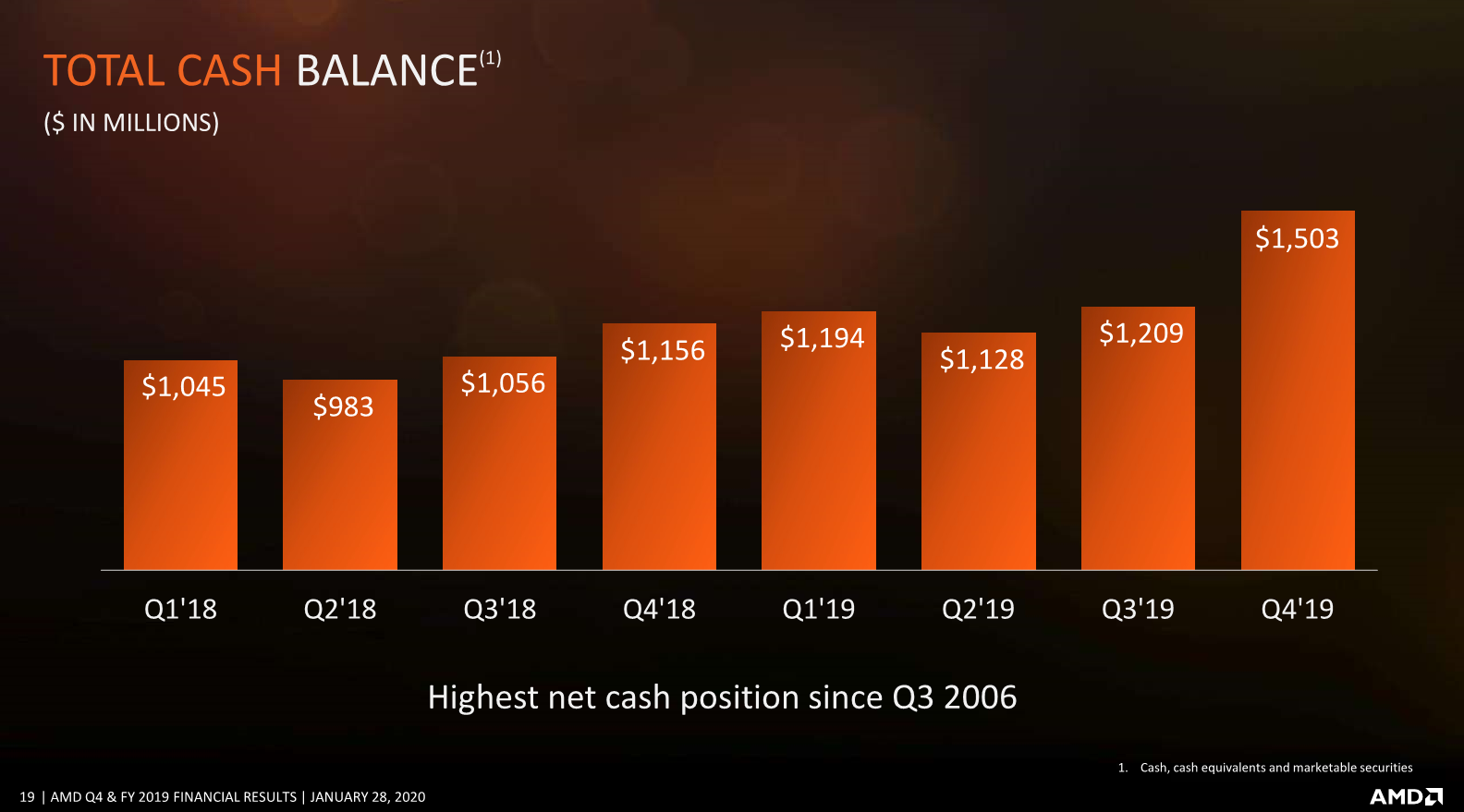

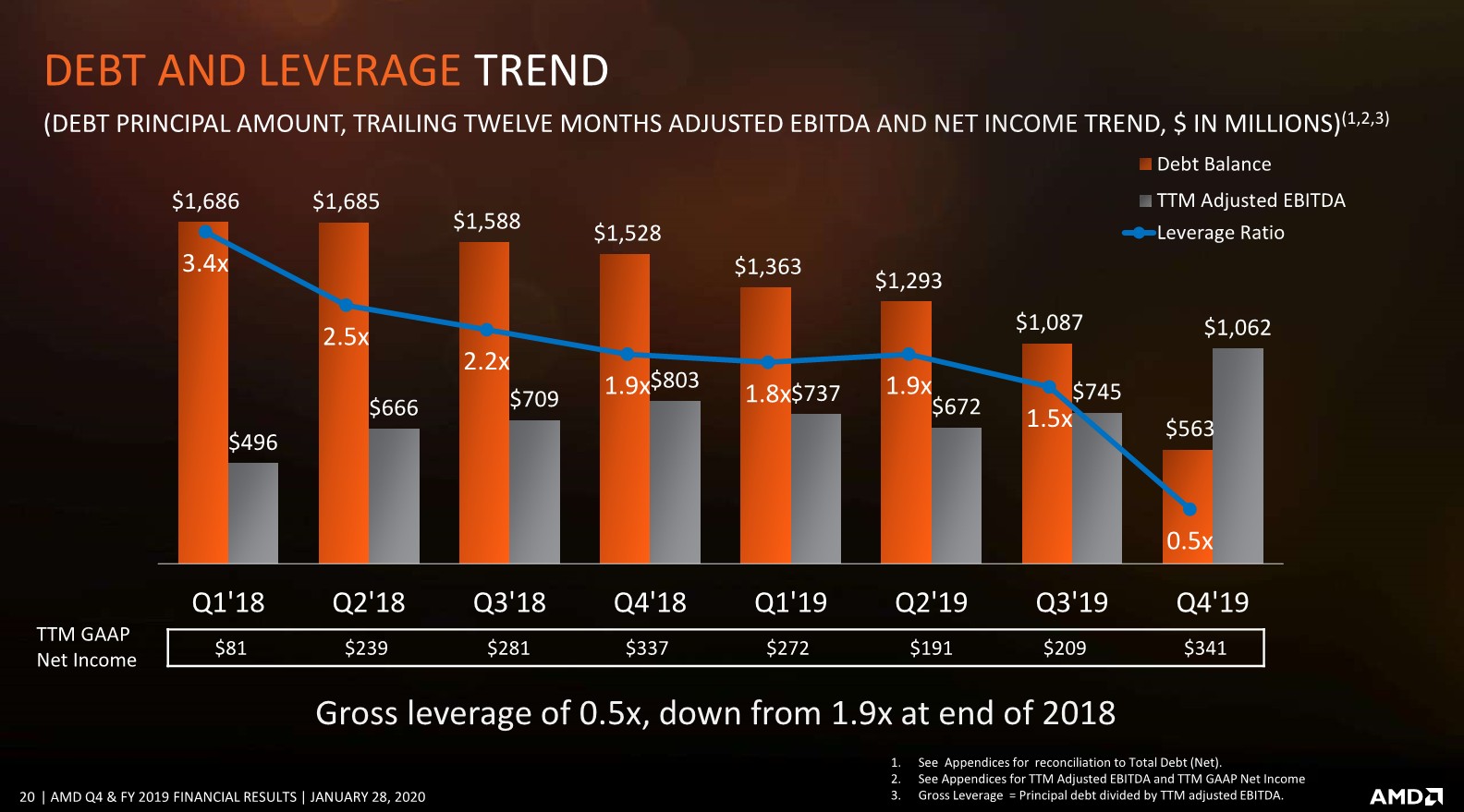

Within Q4, AMD paid down a lot of debt - down from $1087m in 3Q19 to $563m in 4Q19. AMD's strategy here is to pay down debt and strengthen its balance sheet - whether it ends paying off all of its debt is dependent on the types of debt and if there are better uses for the cash.

AMD's Q4 was driven by sales of its EPYC, Ryzen and Radeon hardware, with the Ryzen 3000 series ramping better (after mispredicting demand for products) and the launch of new Radeon 5000 series graphics cards. The EESC gain of +7% YoY is lower than I personally expected, driven by better EPYC sales but weaker semi-custom as we ramp into new consoles in the second half of the year - we have expected EPYC to be a big money spinner for AMD, but we're still waiting for that ramp to happen in significant numbers similar to Ryzen/Radeon as Rome gets a foothold in the server market. We expect the new Threadripper CPUs to make an impact in Q1/Q2, albeit minor given the size of the HEDT market compared to the standard desktop market.

| AMD Q4 2019 Computing and Graphics | |||||

| Q4'2019 | Q3'2019 | Q4'2018 | |||

| Revenue | $1662M | $1276M | $986M | ||

| Operating Income | $360M | $179M | $115M | ||

Computing and Graphics was the lion's share of the earnings gains, with revenue for this segment up 69% year-over-year thanks to strong sales of both Ryzen processors and Radeon GPUs for gaming. Operating income was also up thanks to the higher margins on Ryzen processors. Now that AMD can compete and win on performance, they don't need to sell at such a discount, which is of course what is helping them turn the corner.

| AMD Q4 2019 Enterprise, Embedded and Semi-Custom | |||||

| Q4'2019 | Q3'2019 | Q4'2018 | |||

| Revenue | $465M | $525M | $433M | ||

| Operating Income | $45M | $61M | -$6M | ||

Enterprise, Embedded, and Semi-Custom didn't fare quite as well as the Computing and Graphics side of the house, although year-over-year the results are still up. The 7% revenue growth was helped by higher EPYC sales, but the aging console generation pulled the results down somewhat. It'll be interesting to see how the next gen consoles, with both Sony and Microsoft again announcing AMD internals, will help out over the next year. Operating income for this segment was $45 million for the quarter, up significanly from the $6 million loss a year ago, but AMD still has work to do here. The enterprise and hyperscale sales have much higher margins, but also much longer contract terms, so this isn't a market they will be able to penetrate overnight. They are making small gains, but still have a long way to go.

Expectations from AMD for 2020 is around 28-30% revenue growth, coming from product ramp (such as consoles and Rome), with an overall 45% margin. This margin has two factors - the server margin is going to be more than 45%, but typical console margins are less than corporate average, so that brings it down a little (although operating margin for consoles are actually higher). Looking at the shorter term, AMD is expecting Q1 2020 results to have revenues of about $1.8 billion, plus or minus $50 million, which will be 42% higher than Q1 2019, with margins around 46%.

AMD's official call is set here for 5:30pm ET, so we'll listen in and add anything extra said on the call.

Update 1: Points from the call, in no particular order:

- AMD is expecting its next-generation hardware in client and datacenter to be ramping in advance of the console launches in Q3/Q4 (AMD has clarified that this meant current generation 7nm about to hit the market, as with Ryzen Mobile 4000).

- In 2020, Navi will be refreshed

- In 2020, we will see GPUs built on next-generation RDNA

- Half of AMD's revenue is built on its 7nm product portfolio

- Semi-custom revenue was down 30-50% in 2H19 due to end-of-cycle consoles

- Current inventory is at $1 billion, which is down 6% from last year

- Trailing 12-month EBITDA is $1.1 billion

- 80% of semi-custom revenue for 2020 is expected in the second half of the year due to console launches

- Semi-custom revenue is expected to peak in Q3 for 2020.

Here is the AnandTech transcript of the call. Please link back to this page if you quote parts of the transcript.

Q&A

Bank of America Securities: Lisa, for my first one, you mentioned the goal is get to double digit market share in servers by the middle of the year. I'm just wondering how the visibility is around achieving this target. What's driving it? Is it just more instances at existing cloud customers, and as part of that, do you also have a shared target for exiting this year?

Dr. Lisa Su: We are very pleased with how Rome is ramping. You know, we've been in market now four to five months. With the cloud guys we have visibility in the public facing instances as well as what they're doing in terms of internal workloads. What we see is the breadth of the overall workloads that they're using Rome with is expanding.

On the enterprise side, with the full portfolio of our partners (HP, Dell, Lenovo, and the ODMs), we see a significant increase in the overall enterprise pipeline that we have for Rome. So we're very focused on continuing to grow share in the data center market, and we feel good about our mid-year market share targets. In terms of end-year market share targets, we'll talk a little bit more at our Financial Analyst Day. But certainly for 2020 we're very focused on growing our overall data center share.

Q: For my follow up, Lisa, how should we interpret the impact of capacity shortages at your main competitor? Have you seen any benefit from that? If not, why not? And then kind of Part B is [that] Intel did say that they plan to expand capacity later this year and will focus it more on the PC client side and try to reclaim market share. What effect will that have on the pricing in the market and does your full year outlook take any potential impact of that competition? Thank you.

LS: When we look at the PC market, we finished 2019 very strong, both in mobile and desktop. I think that's primarily on the strength of the product portfolio and the expanding customer platforms that we have. There are some discussions about 'pockets of shortages', but as I said before we've been on this steady increase in market share now for the last eight quarters, and we believe we gain share in Q4 as well. So I think what we see is just the portfolio getting a lot stronger. As we go into 2020. I think we are enthusiastic about our products. In addition to the Zen 2 based desktop products, we've added Zen 2 now in the notebook portfolio, and we'll have that for the full year of 2020. So I think our outlook expects growth in all businesses, including the PC business and we remain very focused on expanding our market presence in both consumer as well as commercial PCs.

Goldman Sachs: I was hoping to better understand some of the key assumptions behind your full year guidance for both your PC business as well as the server business. Can you talk to some of the TAM (total addressable market) assumptions that you're making and the market share assumptions for the full year?

LS: If you look at the PC market, I think the discussion so far has been to call 2020 flat to maybe down slightly. There has been some concern raised about the 2H20 perhaps being weaker than normal seasonality, just due to some of the enterprise refresh cycles that are strong in the first half. We're viewing it as flat, flat-ish, maybe down very slightly. That being the case, back to the comments I made before, I think we feel very good about our product portfolio. Especially when we look at our notebook share, and our relative opportunities to gain market share, the strength of our Ryzen 4000 series products is significantly stronger than previous generations and the platforms are also significantly broader. So we feel good about that.

In the data center market, again, I would say that the growth of computing continues. From our standpoint we see it as a good market environment for data center in both cloud as well as enterprise. When we look at our full year revenue guide of approximately 28% to 30% for the year, the highest growth from a percentage standpoint will obviously be server, given the expectations in that market. But we expect all of our businesses to grow nicely in 2020, and that's just based on where we are in the product cycle and the visibility that we have with customer design wins, as well as overall competitiveness.

Q: A quick follow up on gross margins, AMD is guiding Q1 gross margins to 46%, and then 45% for the full year. I appreciate your semi-custom business is at a low point in Q1 and the ramp is in Q2, and more more so in the second half, is probably dilutive to corporate margins. If you could walk through some of the puts and takes from a gross margin perspective for the year, that would be helpful. Related to that, if you can compare and contrast the gross margin profile of your semi-custom business going into the next cycle versus the past cycle that would be helpful. Thank you.

Devinder Kumar: Overall from margin standpoint, you got it right, we are guiding to the 46% in Q1, and then the semi-custom business, as we've said, is typically lower than the corporate average. As that product ramps in the second half it will have an impact on gross margin. The guide for the year is at 45%, so we feel good about that, having ended 2019 at the 43% level.

From a puts and takes standpoint, it's really about product mix. Lisa talked about the businesses ramping and growing in 2020, with the 28-30% growth in revenue. The data center, as we've said before, is above corporate average. The client gross margin is around corporate average, and some graphics and then the semi-custom business has below corporate average margins. That mix of revenue as it ramps throughout the year will obviously have an impact on a quarterly basis. From an annual standpoint, we feel pretty good to the guide at 45%, in particular with the 7nm products ramping as we get through the year, and that obviously benefits the gross margin. Lisa, do you want to chime in on the difference between generation to generation?

LS: As you said the semi-custom margins tend to be below corporate average on a gross margin basis, although on an operating margin basis, given the contribution from our customers for the R&D, it's actually quite good. As it relates generation to generation, the way to think about it is that in the first year of a console ramp, you would expect the margins to be on the lower side. That's true no matter what, just because you're just starting to product ramp, and you should expect that the margins will get better as that ramp continues over time.

Cowan: I wanted to just start with a question comparing and contrasting a little bit, that AMD is maybe a little weaker than some of us had modelled, and I guess due to the console stuff for Q1 and the guidance of 28-30% growth for the year. Maybe you could just sort of lay out the year a little bit at a high level and just how you guys are sort of thinking about it coming together.

LS: We're pretty excited about 2020. You know, it's a strong year for us, certainly with the expectations of 28-30% revenue growth. We do expect all of our businesses to grow. I think relative to the Q1 guide, if you look at Q1 as an absolute number it is up over 40% year on year, even with semi-custom revenues very low in Q1. That should give you an idea of the strength of the rest of the business.

From a sequential basis Q4 to Q1, it's what we said on the call - there is some bit of normal seasonality, as we are consumer focused in our PC portfolio. So you expect that would go down from Q4 to Q1. Then we do have the factor that the semi-custom profile when we're doing a product transition has the revenue very low in Q1. It then starts ramping Q2, but it's very heavily weighted in the second half of the year. So you should think about semi-custom for this year that over 80% of the revenue for semi-custom will be in the second half of the year compared to the first half of the year. So overall, we think a very strong year, a little bit of re-profiling of revenue, particularly as it relates to semi-custom and we look forward to executing it.

Q: It looks like on the operating expense side, you're going to be up in a neighborhood of mid 20s for the full year in the annual guidance that you outlined. Maybe you could talk a little bit about the focus of that - is it branding and marketing in the PC and server spaces as you grow? Or is it in other areas in R&D? Then secondly, I think you guys had disclosed the data center revenue mix, of GPU plus server in prior quarters, and if you have that number handy, that'd be really helpful. Thank you.

DK: Let me take the second one first. With the data center it's as we said in the past it is mid-teens of revenue, and this quarter it is around the same mid-teens of the total revenue and I'll point out that it is record revenue in the quarter, so that's pretty good about that. We feel pretty good about having mid-teens revenue in the data center, combined server and data center GPU on revenue of $2.1 billion.

As far as OpEx is concerned, our guide for the year is about 28% of the revenue. You are right, fundamentally the investments are in R&D and go-to-market, and obviously the business is growing, so there's investments needed to go ahead and grow the business from an absolute standpoint. We feel we can manage it to about 28% of of our revenue overall for the year.

LS: The only thing I'll add to that is that for the data center revenue, particularly in Q4, it was very heavily weighted towards Server CPUs, just given some of the lumpiness of the data center GPU revenue.

Jeffries: I think it's impressive that the cash that you generated 10 years ago, you were $4 billion in net debt, and now you are net cash positive - I didn't think back then we'd expect you to be here! But how should we think about capital structure going forward? For the $440 million in cash flow from operations, I had a challenge reconciling it - can you share the biggest two or three sources of cash? For Lisa, the last time AMD had a product cycle in servers I think once AMD hit 5% share, you started again share it a 2%-4%, a 400 basis point clip per quarter - what is the right kind of cadence or pace of share gains in servers this cycle? Maybe you could just talk about, structurally, what gaits the pace of your ability to gain share? Is it capacity from your suppliers, is it your own engineering support infrastructure, or is your customers testing and importing workloads? If you could give us a framework to think about that, I think that would be helpful. Thank you.

DK: You do have a long memory! So do I - I do remember the days when we had the challenge on the balance sheet, and one thing we feel good as we end 2019 is the strength of the balance sheet, and in particular the net cash position. We haven't been in this position in many, many years, as we pointed out in the prepared remarks.

From a capital standpoint, and with allocation priorities investing in the business, the revenue is growing significantly in 2020 is what we're projecting, at 28 to 30% over 2019. Also we want to invest in the roadmap to go to market and everything that's needed with the revenue ramps as significantly as it is, going from year over year. So that's really the allocation priorities.

From a viewpoint of where the $440 million comes from, you know, higher revenue, especially when you look at the revenue in Q3 and Q4 of 2019 compared to the first half of 2019, we they did go ahead and buy the inventory to go ahead and support the higher revenue. As you know, when you sell the revenue in particular, when it ramps up, you know, as a debt on better margins, it generates the cash. That's why you have the $440 million operating cash flow

LS: As it relates to the server rate and pace, I think the most important thing for us is when we look at from the time of announcement, or time of shipment, to how customers actually deploy and trying to shorten that cycle. So when I look at the difference between Rome and Naples, we've seen that time to deploy actually significantly shorten with Rome. In terms of rate and pace of server share gain, primarily for cloud customers it is having them deployed not just a set of instances but ensuring that they get fully built out across all regions in the world, and also adding additional support workloads. So for that it's just time is what I would say. As it relates to enterprise customers, I think the platform coverage that we have with Rome, is significantly broader than it was with Naples. I'm quite encouraged by the strength of the pipeline with the number of customers that are engaged and how they're deploying. I think we're going at a good pace, and will continue to accelerate that as we go through 2020.

Stacy Rasgon, Bernstein Research: First I have a question on gross margins. Into Q1, you said consoles are negligible, with gross margins are 46%, so that suggests that that 46% is basically indicative of the business as it stands without consoles. So does that represent kind of the peak of the gross margin on the current mix [of products]? I'm a little surprised it's not higher, given all the new products in aggregate we're supposed to have gross margins in excess of 50%, and most of the mix today should be new products. So how do we think about the Q1 gross margins in the context of that, and what are the drivers that take it higher from here. Is it basically just the mix of server parts, or there something else that can that can help with that?

DK: Lisa can add, but we talked about product transitions - with the 46% guide in Q1, we recently introduced the next generation notebook products. As product transitions go, you still have legacy product that you sell, before you get converted over to the new technology and the new generation products. The desktop products are ahead of that, from that standpoint, and that did benefit our margin in the 2019 timeframe. And you are right, the console has been negligible revenue in Q1 of 2020, and it does benefit the margin to 46%. From an overall standpoint for the year, it is 45%, and that's because the semi-custom business, which is lower than corporate average, does come back. As Lisa said earlier, we are expecting 80% of that in the back half of the year. But by that time, the new generation products in the other businesses, including data center and client, will be ramping all on 7nm and that should have the gross margin to offset some of the impact that we have on the semi-custom business.

LS: We don't expect the client notebook mix to fully cut over to 7nm until later in the year. In terms of opportunities to improve margins, it is definitely about product mix - so a higher mix of server as well as Ryzen 7 and Ryzen 5 versus some of the legacy products.

Q: If I sort of squint to the second half, it seems to me you're probably guiding it implicitly $800m to $1b over the second half of 2019. How much of that do you think is console versus non console, because it's not hard to get a console number, especially in the beginning of a ramp as it's not that far off that that initial number, which doesn't leave all that much room to ramp the rest of the business. So is this just conservatism or what else are you expecting here? How much of that second half do you think is console versus non-console?

LS: I think as I perhaps answered one of the earlier questions, when I look at the full year at 28%-30% revenue growth, we expect server to be significantly above that, and then the rest of the businesses are all going to grow nicely. You would expect significant double digit growth in the client business as well as the semi-custom business. Overall we see the aggregate of it to be a very strong year. So it is not all console weighted, if that's if that's what you're asking.

Q: Wouldn't you get that just from the nature of the ramp that we saw in 2019? I guess I'm trying to sort of normalize second half the second half with a strong double digits in second half versus second half growth across all the businesses.

LS: So what we said in 2019 overall we grew 4% on an annual basis, but excluding semi-custom, we grew over 20% through all the rest of the businesses. If I do that same type of calculation, excluding semi-custom for 2020, we would still say the rest of the businesses would grow greater than 20%.

Instinet: You said the sequential decrease in the quarter is driven primarily by the dropping of game console chips. Does that mean that you expect your microprocessor and graphics revenues will be flat sequentially? Or if not, roughly, what does your guidance team in terms of percentage say for PC processes and GPUs? Do you get server processes sales rising sequentially?

DK: I don't think I said specifically that Q4 to Q1 is all due to semi-custom, that obviously hurts the margin, but there is a product mix underneath that, especially with the notebook products that we talked about that are moving to seven nanometers.

Q: About revenues from December into Q1, the sequential drop. Can you give us some idea - I mean there's a big chunk that is game consoles, but what about the non-game console part of it?

DK: It seasonality in the business. We have the consumer weight from a revenue standpoint in our CG segment, and as we go from Q4 to Q1 you do get seasonality coming into play. Typical seasonality is what is driving the other portion of the decline in revenue from Q4 to Q1.

LS: I think what you're asking is, you know, we would expect that the Computing and Graphics segment would be down sequentially due to seasonality, and we would expect that the server CPUs should be up because we're continuing to ramp those processors sequentially.

Q: Lisa, can you give us some idea of what new GPUs you're expected to launch to the rest of 2020, for PCs and for data center?

LS: Yes. In 2019, we launched our new architecture in GPUs, it's the RDNA architecture, and that was the Navi based products. You should expect that those will be refreshed in 2020 - and we'll have a next generation RDNA architecture that will be part of our 2020 lineup. So we're pretty excited about that, and we'll talk more about that at our financial analyst day. On the data center GPU side, you should also expect that we'll have some new products in the second half of this year.

Morgan Stanley: You talked about consumer graphics as being below the corporate gross margin. I know you've historically had a high cost structure because of high bandwidth memory, but as the portfolio increasingly doesn't use high bandwidth memory, is there the prospect to improve that for consumer GPU to be closer to where your competitors close margins are?

DK: I don't think I've actually said that - I said some of our graphics products are below corporate average from a gross margin standpoint, in addition to the semi-custom have been below average.

LS: To answer your question in terms of what we expect in consumer graphics - We're investing in consumer graphics, and we think gaming is a very important segment, whether we're talking about consoles or discrete graphics. The work that we're doing around the RDNA architecture, and the future generations of RDNA architecture, we believe will continue to improve our offerings for both consumer graphics as well as data center graphics.

Q: With the new console builds, you mentioned that that starts in Q2, but it's mostly in the back half of the year. As you think about that opportunity from a unit standpoint, is it the right way to look at it with sort of similar number of units to what we had in the first year of the current console cycle? Or does the compatibility that you bring when you have an x86 CPU with little bit more similarity between the consoles - could that point us to a sort of a better console unit market in 2020, as we saw six years ago? How are you thinking about it?

LS: We do think there's some pent up demand for the next generation of consoles, you know, without forecasting what our customers are planning, I would say they're both planning for a strong first year and we'll have to see how things develop as we go through the ramp. But the overall sentiment is that there has been, you know, let's call it a lull in console sales in the second half of 2019 going into 2020, for some of this anticipation of the next generation.

Barclays: I just want to make sure I heard you right - I thought you said that semi-custom as well would grow double digits, I just want to confirm that. Just following on, I don't know what the units are going to be, but is there a fee story to lay on top of that equation as well?

LS: I did say that somebody custom should grow double digit as well. It's a strong year for us. Then as it relates to content, it's fair to say that there is additional content in this generation versus previous generation.

Q: On the gross margin equation, is there a way to talk about the mix of 7nm that's a big tail when it still seems early days, at least across some of your products? Is there a way to kind of think about the whole company and what the mix of 7nm is?

LS: We just completed the fourth quarter and it was a very strong quarter for us - record revenue for the company. I would say about half of that revenue was 7nm-based and the other half, you know, is not yet. There is still a significant ramp as we go into 2020. But we're pleased with how quickly we ramped in 2019.

Credit Suisse: I want to go back to the gross margin bridge from Q1 to the full year - I want to make sure I understand that the drop from Q1 to the full year, is that 100% being driven just by gaming coming back more aggressively in the back half of the year? Or have you baked in anything for either pricing competition from the number one guy out there, or some share shifts? How do we think about that? Is it all about gaming?

LS: I think if you look at it, the predominant factor if you're talking about Q1 guided 46% versus full year at 45%, it's just as we wrap those consoles, there's some there's some impact of that. As it relates to the pricing environment, we're expecting a competitive pricing environment, and that's the way we built our model. We've always expected that the competition will be very aggressive on both the CPU as well as the GPU side - that is part of the inherent model or for the company.

Q: You guys have a ton of goodness on your immediate plate on the server side and the data center side, just with the workloads you're going after. But I'm kind of curious - you answered an earlier question saying you expect more GPUs for the data center and I don't want you to pre-announce product, but how should I think about your positioning for AI as a workload and acceleration? Given some of the heavy lifting that NVIDIA had to do around CUDA, how do I think about the investment there? Is this an area that you think you have some unique IP that you can bring to, or how do I think about that over the next couple of years?

LS: I think that's actually a good way of talking about the opportunity. The CPU opportunity is very immediate and in front of us as we look at the opportunities with Rome and the expanding opportunities. I think the data center GPU market continues to be an important growth vector for us and I call that over the several year horizon. When you look at the opportunities that we have, when we combine our CPU and GPU IP together, they're very, very strong. For example this is the reason that we won the Oak Ridge National Lab, the supercomputer with Frontier, which were actually both a CPU and a GPU win. With some of the optimization that we've done with that overall system, we think that there are additional opportunities like that, as well as machine learning and AI opportunities. Our focus there has been to work with large cloud providers to optimize the machine learning frameworks. We had some key milestones that we completed in the fourth quarter, that will continue to be a focus for us in 2020 and beyond.

Q: Is it fair to say that some of the GPU data announcements this year go beyond just the cloud gaming market?

LS: Yes. I think you should expect that we will have additional customer announcements outside of cloud gaming.

UBS: You said over the year that revenue in semi-custom would be in the back half, but how does that breakout between September and December? I'm asking that because I'm trying to see what the gross margin will be exiting this year if you strip out semi-custom - could it be 50% exiting the year?

DK: It's hard to break it down that way. We are in the initial stages of planning for the ramp, and you're asking about Q3/Q4 - we are projecting about 80% of the semi-custom revenue growing double digits year over year in Q3 and Q4. Typically when we have this new console launches, our peak quarter from a revenue standpoint in semi-custom will be Q3. But Q4, when you talk about the ramp of the product, especially in the first year of the ramp, it's hard to project how much it will be and then what the impact will be exiting 2020 from a gross margin. Especially if you ask about excluding semi-custom. Maybe as we get close to that and talk in about three to six months, we can probably give you a better idea of that.

Q: Can you talk about what your [market] share targets are for the year in PC? I think you're 17-18 in notebook, 14 in desktop - can you talk about how much do you think that you can gain this year given all the moving parts with the shortages and whatnot?

LS: I'm not going to forecast a market share target for 2020. I will say though if you take a look back at the last eight quarters, we've been on a fairly steady share gain in PCs, somewhere between, depending on the quarter, 50 and 100 basis points per quarter. That changes between desktop and notebook. I think we grew somewhere on the order of four points of share. We believe that we still have additional opportunities; particularly our focus is going to be notebook as well as commercial and, you those are good opportunities for us and play well to our new Ryzen 4000 Mobile processors.

RBC Capital Markets: For Q4 it looks like semi-custom is probably down 50% sequentially or somewhere around the range. Am I least in the ballpark? Secondly, from a server perspective, how much of your revenues are going to be cloud versus enterprise? I think that's one of the bigger debates and I don't expect you to give specifics but anything you do to help us understand what should be the mix between Cloud and Enterprise for 2020.

LS: You're right - when you look at the semi-custom business in the fourth quarter, it was a bit softer than originally anticipated. We had originally said last quarter that we thought the second half of the year would be down high 30s - we were actually down more than that for the second half of the year and for Q4.

As it relates to the mix of cloud versus enterprise for 2020 - it will move around from quarter to quarter. But I think the best guess at this point is roughly even between the two.

SMBC: On the supply side, you are guiding for pretty strong growth here. I'm just curious, have you already locked in the supply for 7nm, and as we're going to second half of the year, especially as you ramp the game consoles, I believe that those die sizes tend to be very large. I'm just curious how you are feeling about your supply situation. Thank you.

LS: TSMC has supported us very well through the first couple quarters of our 7nm ramp here in 2019. I think as we go into 2020 there will certainly be a significant growth for us in 7nm. Our current visibility supports the revenue guide that we gave you. It is fair to say that wafer supply is tight and it's really important for us to be planning with our customers and that's what we're working on.

123 Comments

View All Comments

TheJian - Sunday, February 2, 2020 - link

LOL. It means a lot. Not everything as there are a TON of numbers you should be looking at if you're serious or care about losses. The PE today tells me run for the hills with a bad year prediction that won't drop it. They should be at ~65 PE today with this Q report, and heading for teens with next Q or two as they ramp higher margin stuff (64c hedt/servers will do it). But it looks like they may be planning ramps of console crap instead of REAL chips ;) So single or barely double digit crap instead of REAL margin products that make REAL NET INCOME. TTM of 200m NET on 6B Rev in your best product year in a decade should have all of management fired...LOL. Your $500 console isn't worth squat compared to a 7K chip (even that massively priced wrong), so why do you keep chasing poor people AMD?Stop reading tech sites for stock analysis. READ STOCK sites. Problem solved. Make sure it's not just some dumb contributor (like me getting paid nothing, knowing nothing about me?...LOL Trust but VERIFY everything in money), instead of someone REAL with credentials and years of a record you can look at. If you want to make money in semi, you should probably have access to something like JPR/MPR or you will be doing a lot more work than needed (or translate a lot of asian stuff). 100K in NVDA today will get you 20K free in the next year. JPR at $5K is cheap if you do it with a few people from say, your work, who also trade stocks or MPR for a year at $1500 ($375 split 4 ways with co-workers). Never mind if you knew what you were doing a few years ago and bought at ~12-22 like we did (but ran way early...ROFL)...Heck nvida was $150 in the last 6 months multiple times and over 1/2 off a year ago again. PE and a few other numbers are all you needed to run at the highs ~year ago. NVDA/MU/AMD should all be stocks people run in and out of every few years if numbers allow it. They all basically long term channel all the time. Between the 3 of them you can be in or out of something making wads yearly. They usually don't all run in tandem for more than a short period of time. Look at a 5yr-10yr chart on all of them. If you're reading tech sites (product into) and stock sites (reports etc!), it is easy to make money on these and many more every few years in not yearly (they all have cycles to some extent easily seen. and they all have hype stories too). IE, NV about to release new gen on new fab tech and profit already reversed and will likely reach old net levels this Q and set records from here on for a bit at least (AMD has to answer with big navi and win or no stopping the train). If you thought it was worth $290 before it's not hard to see $300 coming this time. I'll say likely more in a few weeks probably as I do expect a record, but wouldn't be on it this time. The next Q will have 3 months of 7nm in it probably (piling up launch chips now no doubt), and we will see a record for net income. I'll be shocked if we don't see $300 by Q1 or before next year (I expect more, but will wait for product info before saying buy on that). Only a war or nature can derail this IMHO.

Watch for NV's PE to go to teens shortly as NET income goes back to records. I predict a record for the quarter after next (if not this coming Q). Sell AMD (last week...LOL) and buy NVDA. Collect 20%+ in a year or less. You're welcome. AMD will lose to whatever NV puts out on 7nm watt/heat/noise and perf wise, so clear for a year from NVDA. Intel not on the map until maybe rev 3. Rev 1 Intel is already dead on arrival...LOL. See linus facepalm vid recently about their gpu. Raja is not capable of making a gpu that beats NV engineers (or money?, both?). AMD keeps choosing HBM which kills every big consumer card margin also. If you choose expensive and useless, you make nothing. NV went GDDR5x and rockets to record quarters because it was EASY to make, in quantity, and fast enough for victory without risks of shortages or costs! SMART. AMD should not be using HBM unless the product actually warrants the use for REAL. If the competition is beating you with cheaper stuff you're doing it wrong (stop using HBM on anything consumer!). Repeating said mistake should=FIRED.

Again, not saying PE is everything, just one of many things you should be looking at. If you think it is absolutely meaningless, you should not be buying stocks. You only need a few numbers with that PE in this case to tell you RUN like mad from AMD (for a while? LOL), they don't deserve current valuation with future predictions they made for a year! In a year I'll be wondering why you are at 200+PE still apparently. I'll have to see if the next round of products are priced FAR better before I go back into AMD. If they had not priced so dumb for the last year, this whole report would have been massively different and so would the PE, and the stock would not dive on your Q report.

It moves for a reason, lots of them if you know what you're looking at and it isn't hard to predict given all the data you have per Q on companies today (and their competition). I'm reading text not even in my language much of the time for shipping info, fab info, etc etc. You can literally read to death on any stock these days. If you pick badly today 90% of the time it's lack of homework. No trailing stop on NVDA for a while (290? maybe then depending on AMD response to NVDA march gpus) :) I expect 7nm to push NV well above 1.2B net for a Q shortly, and that will cause $300 on that report or weeks after. Nothing to stop new records coming and teens PE ratio. AMD on the other hand, all baked in, according to themselves. You can see it in the questions too...But, but, margin, uh, er, console, uh, all new products, uh, what, why, how...uhmmm....? Where 1B Q net? NV pulls 1B a quarter now on GPU only (tegra makes nothing still), do the math on AMD. You are pricing wrong. NO, looking at Intel, market share for all, you are retarded AMD. The guy should have just asked if you are mentally handicapped or something yammering "how could you F this up?" as he walks off. :) Fire your "modeler" for pricing. Revenue up 30% next year, but pricing? You added 2B in revenue the last 2yrs and gained nearly NOTHING in NET INCOME. Last 3yrs and TTM 209m last 3yrs 337,000, 43,000, -497,000. Why the drop TTM? Aren't you ramping all your new stuff? WTF?

I'm going to have to see some price hikes at this point or the next rev pricing leaked. I feel like they'll be worth current value (well, last weeks value) in a year. So not much point in the next 12 months when I can make 20% in NV easily etc. Maybe I change that opinion as we find out what is going to happen with apple's share of TSMC 7nm silicon in more details. Sold most MU until the Q report too. If they don't guide much higher (back to old levels) they will get hit on the report for a recovery that STILL hasn't come quite yet. It's coming (mass profits again) but you can only promise and not deliver a few times before they make you pay even if the reality is changing just around the corner. Big fund managers do this on purpose every chance they get and jump right back in after they tank it and force small runs on a stock so to speak. Long termers like me just ride that crap out usually.

Sorry to disappoint you. I have never worked in fast food. That is a job for teenagers, illegals and people with no skills.

You don't seem to understand what a stockholder is. Naked rage? Weirdo? Raping their customer would be charging massively more than the competition. In this case we literally have the ceo saying they are charging below market value. You are a retard if you don't get the point here.

You don't seem to understand "what the market will bear" and that it is exactly what ALL companies are trying to guess if run by good management. If you are "raping" your customers, by definition you would not SELL a product to many people correct? Only the people who could “afford” to get raped would buy correct? It sounds like you are just sad you're poor and a probably working in fast food and have to beg for cheaper prices :) Start following my stock advice and you'll get FREE PC parts. Like the guy with the FREE CAR in this comment section. He's not complaining about the cpu prices, as it's free anyway along with his next 6 cars apparently (nice work!). Why are you still paying for parts? LOL.

IE, if Intel was raping customers, they would not set record quarter after record quarter correct? I mean, who buys rape? You don't seem to understand the point of owning stock...ROFL.

Wow, no point in calling you ignorant. You are straight up stupid. You think I'm weird for commenting ABOUT the stock, on a stock report mind you, while YOU just attack me and act like the article and the data I put out doesn't even exist :) Don't think you're stupid? OK. Yeah, stupid is, as stupid does. But I just believe you're stupid period :)

Someone like you leads to 20T in debt. Someone like me leads to profit, as close to what they market will bear as I can get :) PERIOD. That is your job as a company leader. The market should dictate how "NICE" you need to be, not your dumb CEO. I didn't say rip people off, I said charge what you are WORTH or change your product mix. You are just too dumb to get it.

Dumping junk is not ripping people off. Switching to a higher margin mix is just good business if silicon is short. Stop working at a fast food joint and none of these prices are raping you. I can afford Titan's every year (waste of money, but I can) and I'm not rich; at least not my definition of it anyway. Do you buy stock to lose money? Again, stupid. At least learn to debate:

Google paul graham's hierarchy of disagreement. Wake me when you learn to debate.

https://en.wikipedia.org/wiki/Paul_Graham_(program...

For the lazy among us, and fast food managers too. Ah wait, they are by definition lazy, as in too lazy to find better work or skills. I want to be a fast food manager when I grow up...Said nobody.

You're giving smart people a bad name...Wait, you didn't claim to be one. OK, all forgiven. So no comment on the data then...Your loss if you ignore it. I lobbed a grenade to see if anyone could stop it from blowing up, yet you didn't get it. Consider my post a trump tweet, or "trial balloon" against my data. He floats a balloon to start a conversation about important stuff, then moves to where he really wanted us to go to begin with as people get it. Smart traders realize what just happened (hopefully gain insight from it, good or bad). Thanks to all for removing any FUD I had about selling...LOL. If you follow my posts (here and elsewhere, stock sites etc), you have been making money time after time. PERIOD.

Jeez, we have presidential candidates (and all fake news, MM) calling the current president a nazi, racist, murderer, comparing him to actual mass murderers, and every other name in the book, unfit for office and on and on. All of this despite the highest economy ever, lowest unemployment for all, highest stock market ever, TWO trade deals nobody could get done, moved embassy, recognized Israel, fighting Iran/China/Russia with ECONOMY rather than war etc etc. But you have a problem with harping on dumb CEO's when a bad report warrants it (I'm not alone, it went down for a reason)? ROFLMAO. SJW's crack me up. For the record though, I'd rather trump make everyone pissed and America rich (I get richer then too), than make everyone happy and USA broke so you can feel good as I couldn’t care less about your feelings. Need a safe space now? LOL. So tight (WTF? So 12yr old) to see all these SJW's attack me and have NOTHING to say about data (in or out of the article...).

I made money. Did you? Not even trying? Why are you here? Go back to reading reviews, this is a quarterly report for stock holders. You just keep working, I'll keep trying to make my money work for me so I can avoid being you. ;) I'll take weird over dumb. I'll take rape over bankruptcy too :) I can recover from rape, not so sure about the bankruptcy. If I have money I can afford therapy for the rape right? ROFL. Some SJW just blew a gasket...One less SJW? Yippee. Back to stock hunting, and bartiromo about to come on :) You've wasted enough of my time and I can type 50

+wpm (60+ on a good day).

Korguz - Monday, February 3, 2020 - link

what the heck did this all say ?????Spunjji - Monday, February 3, 2020 - link

It said he loves the Trump and doesn't brain good.Spunjji - Monday, February 3, 2020 - link

What an asbolute pile. Some highlights for those who understandably don't want to wade through this junk:"...they may be planning ramps of console crap instead of REAL chips..."

"...why do you keep chasing poor people AMD?"

"Sorry to disappoint you. I have never worked in fast food. That is a job for teenagers, illegals and people with no skills."

"You are a retard if you don't get the point here."

"I can afford Titan's every year (waste of money, but I can)..."

"You're giving smart people a bad name...Wait, you didn't claim to be one. OK, all forgiven."

"Consider my post a trump tweet, or "trial balloon" against my data."

"Jeez, we have presidential candidates (and all fake news, MM) calling the current president a nazi, racist, murderer..."

"I can recover from rape, not so sure about the bankruptcy."

In short, standard Trump supporter: unwarranted confidence in own intelligence, inability to stay on topic, thinks bragging about being awesome is the same as being awesome, thinks being offensive is the same as being smart, projecting like IMAX.

My favourite bit was where he came to a tech site to rant about stocks and then told people not to come to tech sites for stock info. A++ goonery.

ballsystemlord - Sunday, February 9, 2020 - link

Thanks for the summation, Spunjji. I find you to be correct.Incidentally, TheJian, if someone doesn't start "chasing poor people" then poor people will not have computers. And I at least value that moral quality of AMD, which they are sadly loosing over time. :cry:

Zoolook - Wednesday, January 29, 2020 - link

AMD could be the largest TSMC customer on 7nm in 2020.Apple, HS and Qcomm has moved on to 5nm for new chips so their volumes will shift away from N7P and N7FF+.

TheJian - Sunday, February 2, 2020 - link

Agreed, I think AMD will be #1 on 7nm at tsmc this year (well at the end that is). I just hope all the silicon goes to higher margin kit, rather than single or barely double digit crap (console like junk). No point in wasting silicon on $100-125 parts that make you $10-15 if you're a player like AMD vs. NV/Intel. You should be making the high margin parts only until it doesn't sell (see Intel), then make junk to add to your bottom line because that is all that is left.I really wish AMD had passed on console like NV, and for the same reasons (let Intel or someone else take that crap on). IT robs from your CORE R&D. It did exactly what NV said it would; killed AMD profits for years, cost fabs, land, engineers, etc. They gave it all up to claim a console victory or two that keeps stealing R&D design after design...They could have been a contender in the cpu race years ago (instead of basically giving up for 5-6yrs), and should not have been dominated by NV for ages either. I hope they choose wisely for the new silicon. They claim gpus/cpus (not socs/apu junk), but we'll see.

$52+ last week. Hope people sold. Likely more down for most stocks as anti-trumpers try to kill his market over this virus crap, fake impeachment etc. Good to be in safer stocks (with no debt) with room to run and good report coming (nvda for example for a while, no loyalty to either stock...should hit 300+ easily in 12mo, likely far less time). I think NVDA will set a record this Q or next and head to 300 again. Easy money if you don't mind the virus ride. The Flu kills ~2500 a year in usa, so miles from this still but that won't stop trump haters from trying to down the market as usual on anything they can. Middle class got 40% on their 401k but dems keep trying to take it down or give it away before you get it. They give it to illegals, welfare, free college, etc etc...Whatever they can do to bankrupt you and put you on welfare for life is their goal (and voting for said welfare for life). Too bad 1/2 the public still watches fake news, although more appear to be waking up as ratings for impeachment etc show complete tanking for dems. Even the debates have terrible ratings.

Spunjji - Monday, February 3, 2020 - link

"I really wish AMD had passed on console like NV"They didn't "pass" on it - they lost the business because of their constant gouging.

"Likely more down for most stocks as anti-trumpers try to kill his market over this virus crap, fake impeachment etc."

LOL

"Middle class got 40% on their 401k but dems keep trying to take it down or give it away before you get it. They give it to illegals, welfare, free college, etc etc..."

Can an admin get a ban on this assclown now, please? He's very obviously just here to spread disinformation.

Lord of the Bored - Wednesday, January 29, 2020 - link

Please take your antipsychotics.You're fired.

haghands - Thursday, January 30, 2020 - link

He really needed this job man. Think of the kids. Oh god I hope he doesn't have kids lol.