Intel Announces Q1 Fiscal Year 2016 Results: Lower Margins Prompt Workforce Adjustments

by Brett Howse on April 19, 2016 11:35 PM EST- Posted in

- CPUs

- Intel

- Financial Results

It was only last quarter that Intel reported record revenues for a Q4 in the company’s history, and only three months later the company is making dramatic cuts to their workforce. With the job cuts only just announced, the company then released their first quarter results of fiscal year 2016.

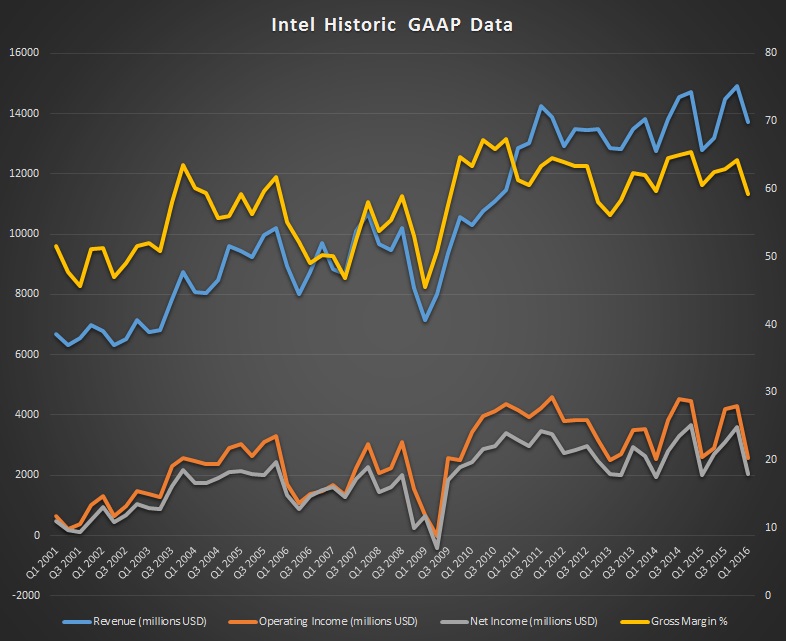

On a GAAP basis, the news is not quite what you would expect for a company that is slashing its operating costs through employee reductions. Revenue for the quarter came in at $13.7 billion, which is up 7% year-over-year. Some of the gain though can be attributed to changes in Intel’s reporting methods, as it has aligned its fiscal year with the calendar year, resulting in an extra week of time for this quarter compared to a typical quarter. Perhaps a more telling result is Intel’s gross margin, which fell to 59.3% for Q1, down 1.2% from last year. Operating income was flat despite the gain in revenue, coming in at $2.6 billion. Net income was up 3% to $2.046 billion, and earnings per share were up 2% to $0.42.

| Intel Q1 2016 Financial Results (GAAP) | |||||

| Q1'2016 | Q4'2015 | Q1'2015 | |||

| Revenue | $13.7B | $14.9B | $12.8B | ||

| Operating Income | $2.6B | $4.3B | $2.6B | ||

| Net Income | $2.0B | $3.6B | $2.0B | ||

| Gross Margin | 59.3% | 64.3% | 60.5% | ||

| Client Computing Group Revenue | $7.5B | -13.8% | +1.74% | ||

| Data Center Group Revenue | $4.0B | -7.17% | +8.64% | ||

| Internet of Things Revenue | $651M | +4.16% | +22.14% | ||

| Non-Volatile Memory Solutions Group | $557M | -14.83% | -5.91% | ||

| Intel Security Group | $537M | +4.88% | +12.11% | ||

| Programmable Solutions Group | $359M | - | - | ||

| All Other Revenue | $50M | -15.25 | -34.21% | ||

Intel also reports Non-GAAP results which exclude certain factors such as acquisition costs, deferred revenue write-downs, inventory valuation adjustments, restructuring charges, and a few other factors. On a Non-GAAP basis, revenue was up 8% to $13.8 billion, gross margin was up 1.3% to 62,7%, operating income was up 13% to $3.3 billion, net income was up 19% to $2.6 billion, and earnings per share came in at $0.54, which is up 20% year-over-year. One of the big factors in the non-GAAP numbers are due to the acquisition of Altera, which was completed early in fiscal year 2016.

The Client Computing group is the largest part of Intel on a revenue basis, and is the one that is feeling the pressure of the declining PC market the most. This segment had $7.5 billion in revenue for the quarter, which is up 2% from the same time last year, but breaking down the numbers we see that there was a decrease in volume of sales of 15%, but the average selling price increase of 19% means there was a small gain year-over-year. Operating income for this segment was $1.9 billion, which is up from the $1.4 billion a year ago. Notebook chips had a flat average selling price, and saw a 2% decrease in volume, while desktop chips sales fell 4% but had a 6% increase in average selling price. Tablet sales saw the biggest hit, down 44% to 4 million units. The tablet market has not matured at the rate initially expected, and Intel has gotten rid of the contra-revenue plan to boost tablet sales, so this is not unexpected. With strong competition from ARM based designs in this segment, Intel is hoping design wins in 2-in-1 devices will help.

The Data Center Group was almost the opposite, with a strong growth in unit sales, up 13% from a year ago, but average selling price fell 3%. Revenue for this group was $4 billion, up from $3.7 billion a year ago, but with the decline in ASP the operating income was only up $65 million to $1.764 billion for the quarter.

Internet of Things posted revenue of $661 million, up from $533 million a year ago. The growth continues in operating income for this new segment of Intel, which saw a 41% gain over last year, and was at $123 million for the quarter.

Intel also has some new reporting segments this quarter. They have added Non-Volatile Memory Solutions, Intel Security Group, and Programmable Solutions Group. The latter is a new segment based on their acquisition of Altera and will be for their expanded FPGA business. The others are branching off from Software and Services and All Other.

Non-Volatile Memory had a drop in revenue of about 6%, to $557 million, and took a $95 million operating loss for the quarter, down from $72 million in operating income last year. The Intel Security Group had revenues up 12% to $537 million, and operating income up to $85 million for the quarter, which is an increase of 286% over the $22 million last year. The Programmable Solutions Group, being a new addition to Intel, only has results from this quarter, which were $359 million in revenue and $200 million in operating loss with the acquisition costs.

Finally, the All Other group had revenue of $50 million, and had an operating loss of $994 million for the quarter. Intel used to have quite a bit of technology under All Other, but with the new reporting groups much of that has been shifted out. It now features operations from the “New Technology Group” as well as restructuring charges, employee benefits, and other expenses.

Clearly with the large layoffs announced today, Intel is trying to refocus its efforts on markets where it can continue to grow. Their success in the PC market has been quite pronounced, but with that major market shifting to slower upgrades and fewer unit sales, Intel is going to try again to go after markets where it sees opportunities. One such market was mobile, but Intel was very slow out of the gate to latch on to that, and we are only now seeing Atom parts on a regular update cadence with Goldmont announced for later in the year. Airmont cores never even found their way into a smartphone SoC, meaning that any Intel powered phones were still the older 22nm cores.

It's unlikely anyone but investors like to see companies shed so much of their workforce, and this could be a big impact on Intel in the future with fewer resources to throw at problems, but it could also mean a leaner, more agile company. Time will tell on that story.

Looking at the immediate future, Intel has forecasted revenue of $13.5 billion, plus or minus $500 million for next quarter, which will return to a 13-week quarter as well. Non-GAAP margin is expected to be 61%, plus or minus a couple of percentage points (and yes that’s pretty vague), and with the job cuts they are expecting to take a one time charge of $1.2 billion.

I think Intel has weathered the slowdown in the PC market better than most companies, but they are not immune to the effects, and today we see them trying to offset those losses and move into new markets to win back some of their margin. We’ll keep an eye on their results over the next several quarters and see how they do. They are already getting 40% of their revenue and 60% of their margin from non-PC segments, so they see a good opportunity here to expand that.

Source: Intel Investor Relations

40 Comments

View All Comments

Donkey2008 - Sunday, May 1, 2016 - link

Agreed.tipoo - Wednesday, April 20, 2016 - link

What's crazy to me is the company everyone used to call the 900lb gorilla of the silicon world, and still is, watched mobile explode for an entire decade now, and still only made minor inroads towards entering the market. The Atoms they produce for phones are just-ok competitors to ARM SoCs of a few years ago.

I think ultramobile spaces are where their x86 decode + ucode ROM die area and power draw start to really show up and hurt them. On huge cores they were trivial, on tiny cores they take quite a lot of the floorplan.

http://regmedia.co.uk/2012/08/29/amd_jaguar_core_f...

patrickjp93 - Wednesday, April 20, 2016 - link

ARM is having that exact same problem now as its instruction set expands. It's hilarious to see people still claiming ARM is more efficient (and thus a great candidate for the server world), but not realize that efficiency comes at a huge cost to performance, and ARM is still leagues behind.Krysto - Wednesday, April 20, 2016 - link

> and ARM is still leagues behind.What are you talking about? In servers what matters is money/performance/Watt.

ARM crushes its direct competition in that (Atoms). Atoms tend to cost twice as much for the same price, and barely have almost equal performance while being 2 node-generations ahead.

Put a let's say $50 ARM server chip against a $50 Atom server chip, both on 14nm FinFET, and let's see which comes out ahead. (hint: it's not going to be Intel).

jwcalla - Wednesday, April 20, 2016 - link

Efficiency doesn't cost performance, it's a measurement of performance to power. Efficiency can allow one to perform better with less power. Consider the move from Kepler to Maxwell. Maxwell uses less power and performs better, with no node shrink. It's just a matter of a better processor design. Whether or not ARM can compete with Intel in that department, well that's a different story.tipoo - Thursday, April 21, 2016 - link

Perhaps you can demonstrate the proof of this. ARM took 64 bit as a chance to do a clean design with ARMv8, and they still limit instructions to 32 bits.This comes worlds apart from the x86 approach of gluing both together.

The proof is kind of in the pudding with phone Atoms performance compared to high end ARM, even comparing costs and power draws.

LiverpoolFC5903 - Thursday, April 21, 2016 - link

The Zenfone 2 was the last Intel powered mainstream smartphone, carrying a chip that was announced in 2014, the atom z3580.You cannot tell me that chip is inferior to an ARM chip apart from meaningless and idiotic geekbench Antutu numbers. Real life performance of the ZF2 is pretty much flawless. The g6430 GPU is adequately powerful and comes close to the 805's adreno 420, which was brilliant for a 300 dollar phone.

Try browsing on chrome on a ZF2 and compare it to your S7s and G5s of the world , you'll notice the difference.

Remember this chip can run a full blown desktop Windows smoothly, that's how powerful it is. I am not getting into the beaten to death ARM vs X86 debate, but the general computing capabilities of this chip is ahead of most ARM competitors.

LorinT - Wednesday, April 20, 2016 - link

This is no fault of Intel -- it's the result of fumbles by the bigger fish just up the food chain; the folks in Redmond. Four tiresome years of tiles, with the hope that the world would somehow think Microsoft's tablet was useful. I find both releases downright confusing. Total wreck of an operating system. The latest atrocity was to limit Windows 7 to run only on older hardware. Of course Intel can't sell new Skylake chips if Microsoft's only useful OS is cripped to only run on Broadwell and older.Let's hope that Apple's new product line gains some popularity, enough to let Intel recover a little from Ballmer's completely botched ideas.

Krysto - Wednesday, April 20, 2016 - link

Or maybe the problem is that Intel tries that to sell Core M "tablet chips" for $200 a piece, making it a HUGE part of the tablet's BOM (iPhones and iPads have a TOTAL BOM of LESS than $200, for instance).doggface - Wednesday, April 20, 2016 - link

You can run win 10 on skylake. Can u not read? Do you not understand words? Please try and keep up. Also, any such decision (which there was not) would be an MS decision. Not Intel. Wow, the stupid is strong in this one.